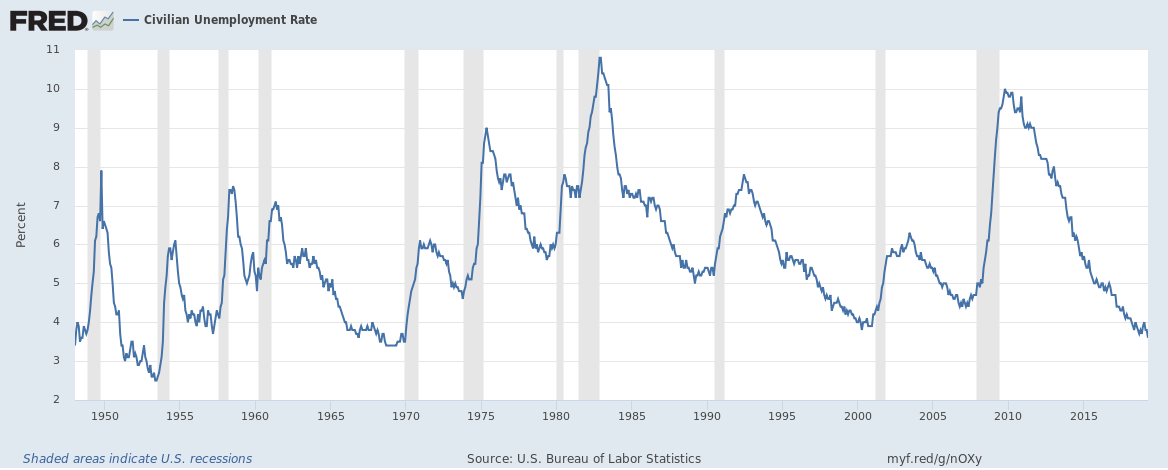

The U.S. unemployment rate hit 3.6% in April 2019, its lowest level since December 1969.

Why wouldn’t it be?

The U.S. unemployment rate hit 3.6% in April 2019, its lowest level since December 1969.

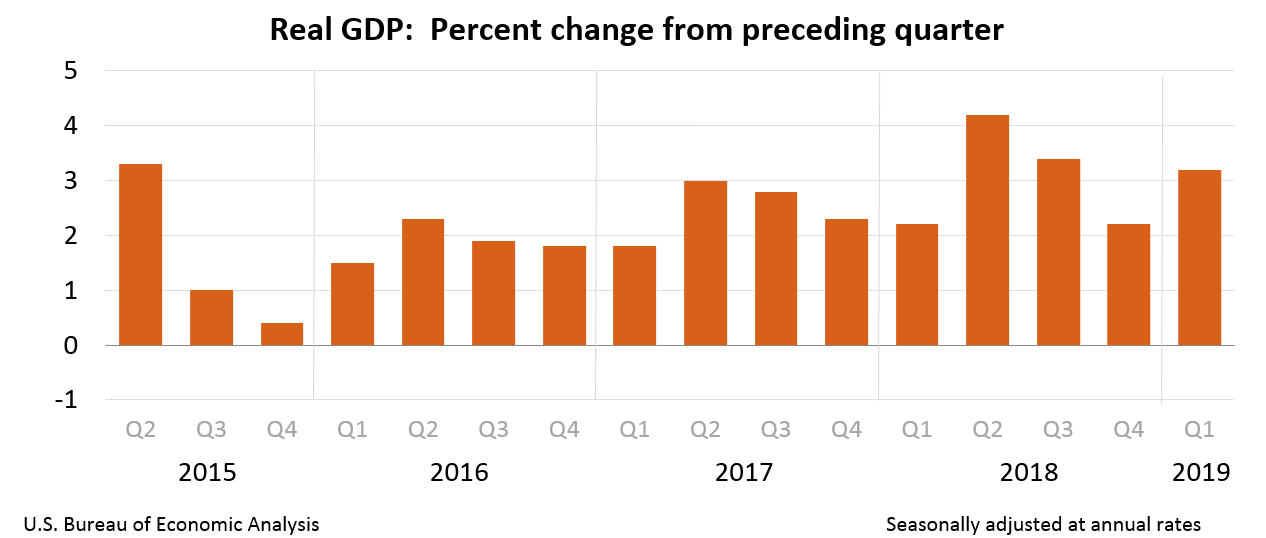

Real gross domestic product (GDP) for the U.S. increased at an annual rate of 3.2% in the first quarter (Q1) of 2019, according to the advance estimate released by the Bureau of Economic Analysis (BEA).

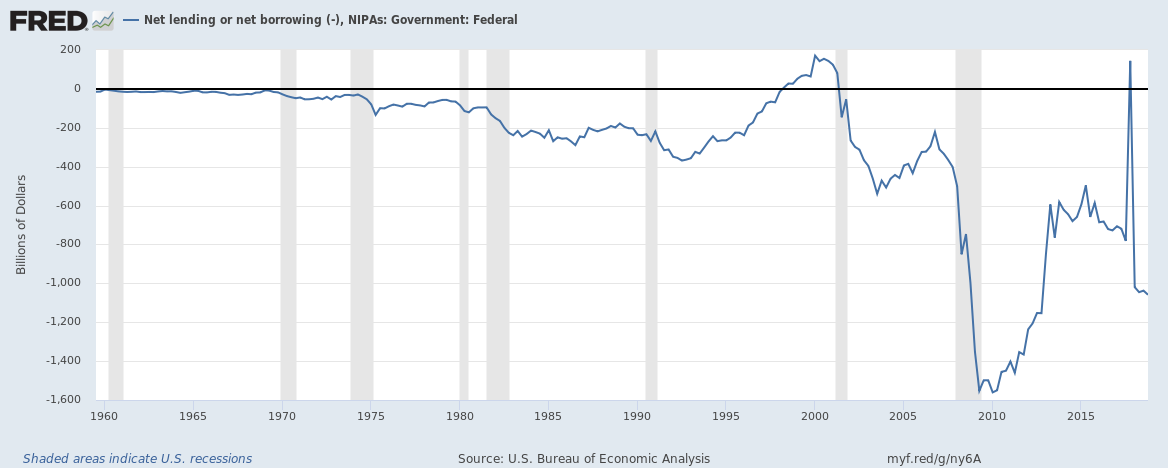

The U.S. fiscal deficit hit an annualized $1.06 trillion in 2018 but relatively speaking it isn’t that bad. The fiscal deficit had hit $1.5 trillion in 2009 in the aftermath of the financial crisis and the current level is the most since 2012.

Continue reading “The U.S. fiscal deficit hit $1.06 trillion in 2018 but is it really that bad?”

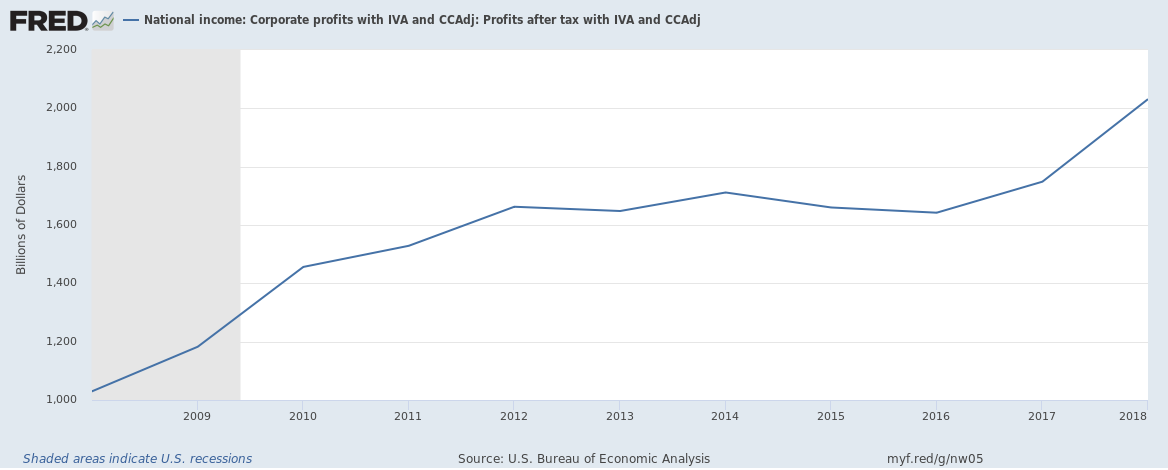

U.S. corporations made a record $2.03 trillion in profits after taxes in 2018,

Continue reading “U.S. corporate profitability accelerated in 2018 growing at 16% … or 8%”

With interest rate rises on hold and signs of a slowing global economy, there have been a lot of noises that house prices globally are falling. We look at how U.S. house prices are looking compared to a year ago.

Continue reading “Are house prices in the U.S. really falling? March 2019 Edition”

We wrote about three slightly different U.S. recession indicators that have been predictive of the past few recessions and have been tracking how near or far are those from being invoked, here’s where we are in March 2019,

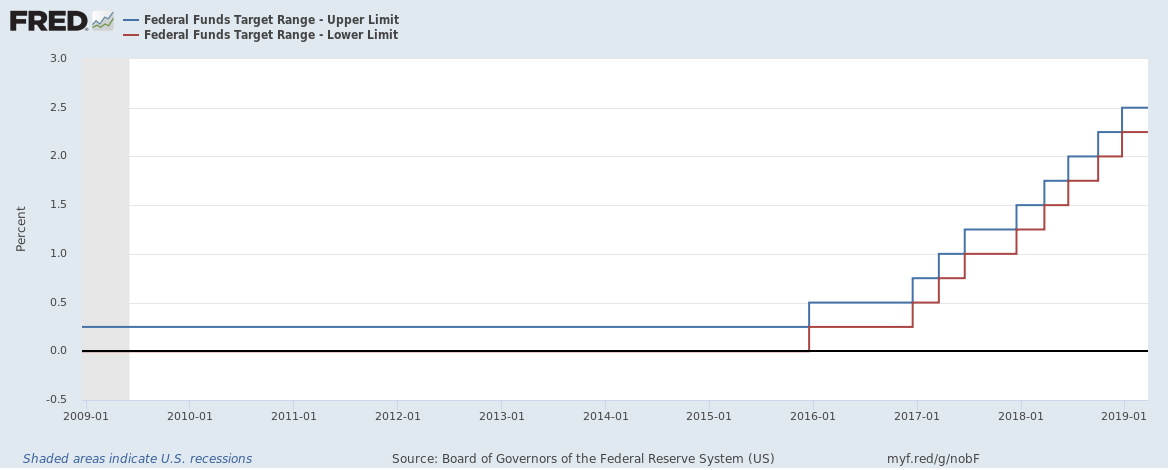

At the start of 2019 we wrote that 2019 will be a year that will be different with interest rate hikes slowing or interest rates even reversing.

Earlier this month the European Central Bank said interest rates would remain at record lows at least until the end of the year and then last week this was followed by the Federal Reserve saying that it does not expect an interest rate rise for the U.S. for the rest of 2019.

The Federal Open Market Committee (FOMC) announced during the week that it had decided to maintain the target range for the federal funds between 2.25% to 2.5%.

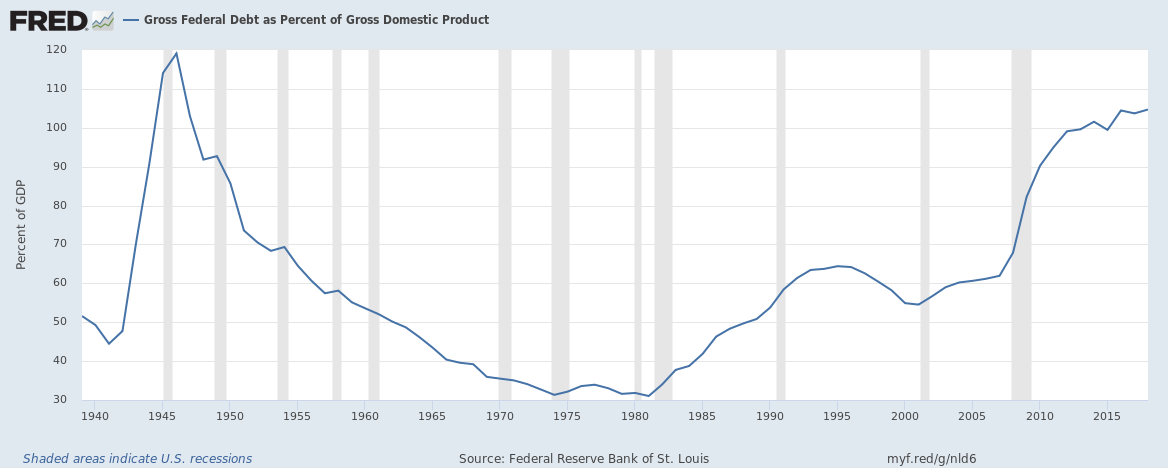

Gross U.S. Federal Debt as percent of Gross Domestic Product (GDP) hit 105% in 2018, the highest since 1946.

Continue reading “U.S. Federal Debt hit 105% of GDP in 2018, the highest since 1946 but …”

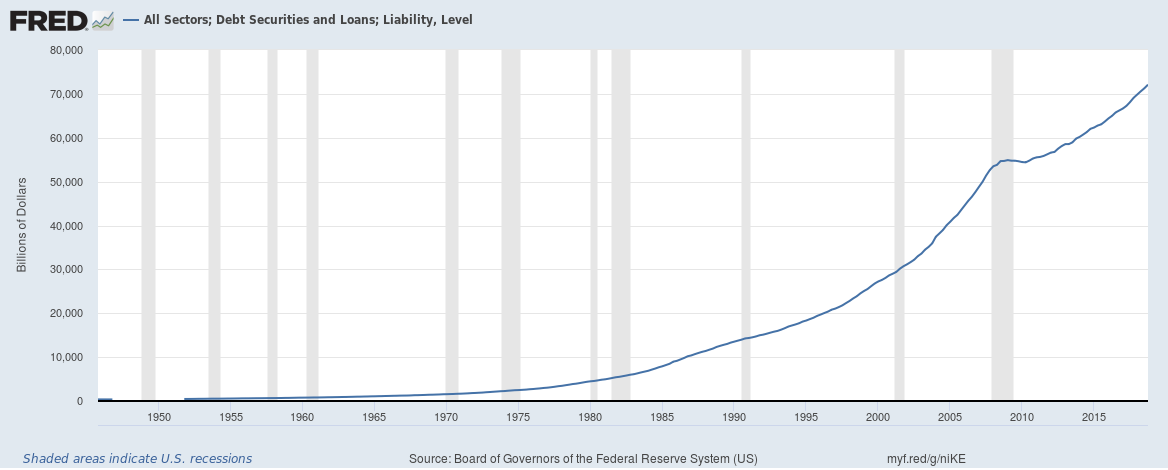

The answer is different on how you look at it – in terms of absolute outstanding debt, growth rates and relative to GDP.

In absolute terms the total credit market or total debt outstanding of the U.S. which includes debt owed by the government (Federal and local), corporations and households stands at $72 trillion.

Continue reading “How big really is the total debt of the United States?”